In this Drill Down: How housing heroes navigate our choppy economy

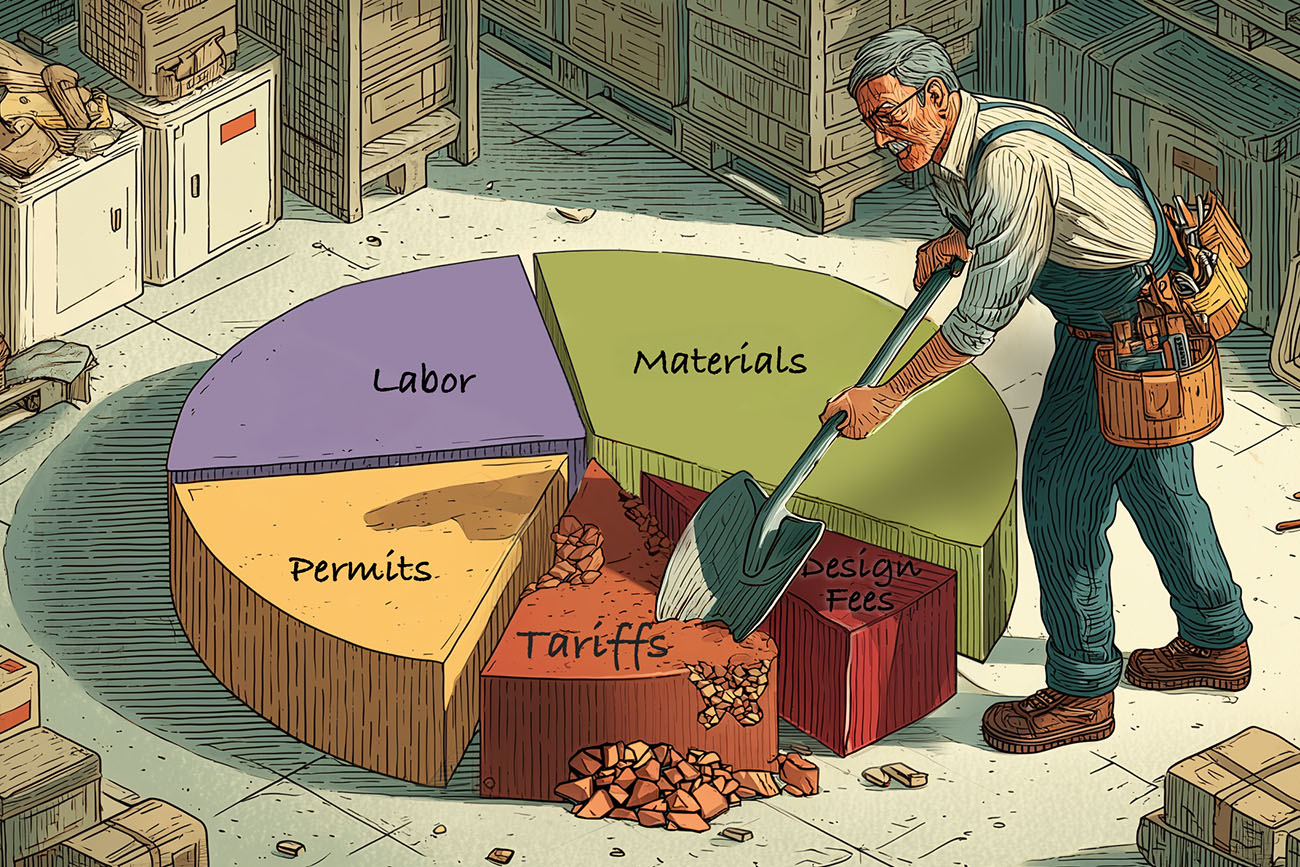

Why homeowners are skipping the backsplash to pay for the roof this year

Practical, not pretty, is what’s driving home renovations this year.

Persistently high home-loan interest rates, stalled home appreciation, and the uncertain effect of tariffs are all flashing yellow for homeowners considering investments in their houses.

“They’re handcuffed to the house because of the rate and their equity. Yes, the buy-sell market is slow, so people are spending on renovations in lieu of selling and moving up,” said one remodeler.

“People have looked at the options and what they’re seeing is houses that also need work. So they’re staying put and making their homes the space they were looking for.” More here: (Source)

The S/M Take:

Oh, the times they are a-changin’. Homeowners – and the remodelers they employ – are now placing their bets on the improvements needed to secure their housing investment, not embellish it.

In more predictable times, Joe Homeowner dreamt of marble countertops, spa bathrooms, and Pinterest-worthy kitchens. Today, with a sleepy resale market and flattening price appreciation, there’s a new calculus at work: risk reduction, not resale fantasy. Upgrades are being judged by future cost avoidance, not visual payoff.

What’s a marketer to do? We suggest a quiet shift toward practicality, where comms indulge less in the dream home and more in the drama-free home. Don’t hold back on the functional, reliable features of your brand. For the foreseeable future, boredom is beautiful.

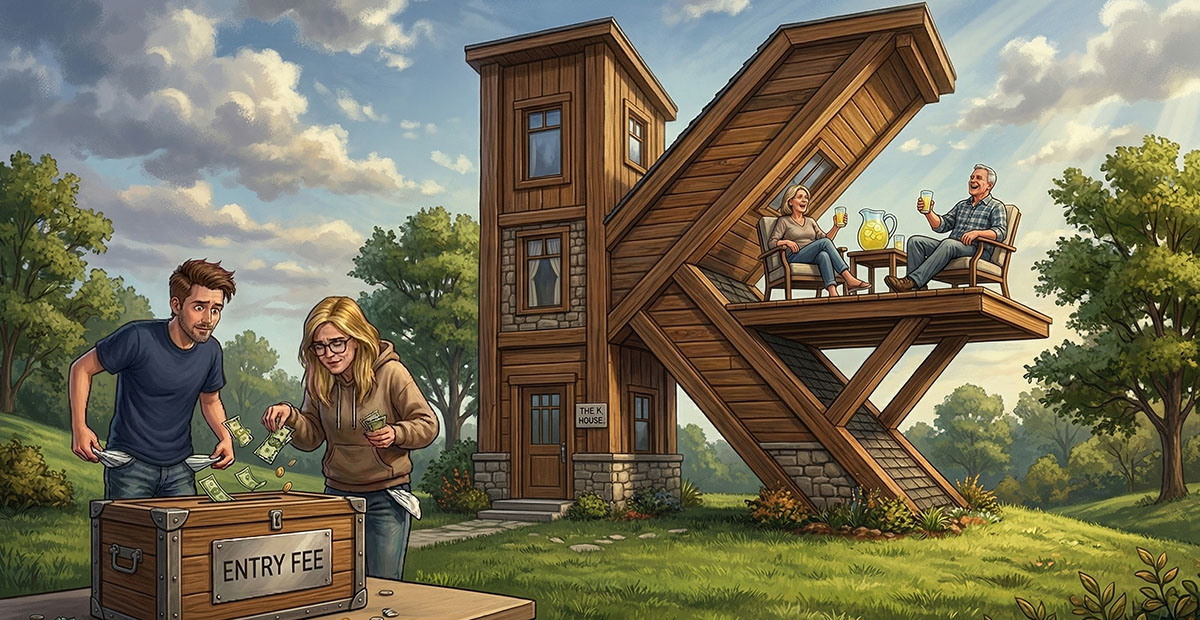

New homebuyers are paying a record ‘entry fee’ to own a home

It's no secret that housing is expensive, but what’s less apparent is the widening financial gap between existing homeowners and those looking to gain a foothold in the market.

Since the COVID-19 pandemic, the U.S. housing market has fractured into two, mirroring the broader K-shaped economy. On one side are the new buyers, paying a record premium to enter the market; on the other are existing homeowners, whose housing costs — as a share of income — are at near-record lows. More here: (Source)

The S/M Take:

The bifurcation is real.

We are now in an era of “incumbents” and “entrants,” and the two cohorts see life very differently. As marketers, so should we.

The incumbents are equity-rich, payment-insulated, and as the story above stated, oriented toward protection of their precious asset.

Meanwhile the entrants are cash-strapped, payment-sensitive, and risk-averse. They will watch every purchase dollar like a hawk, which is one reason that Redfin reports it took a dogged 66 days – more than 9 weeks – for houses to find a buyer in February. That’s the slowest pace in a decade.

So when entrants turn the corner, when they finally break through, we need to meet their moment and help them feel like incumbents faster. That flurry of improvements that new homeowners make? It needs to be built on value creation and durability.

Confessions of a homeowners insurance exec

As insurance markets tighten across wildfire, wind, flood and freeze zones, mitigation is shifting from an optional upgrade to a baseline requirement, forcing homebuilders to rethink how resilience factors into construction, sales and long-term strategy. Rising reinsurance costs and record catastrophe losses have made carriers more selective, underwriting communities individually and rewarding demonstrated risk reduction.

In this conversation, a leading insurance executive explains how wildfire standards, smart water shutoff valves and embedded insurance can support stronger insurability. More here: (Source)

The S/M Take:

Raise your hand if you had “insurance underwriter” on your target-audience bingo card 10 years ago. Nobody? Yeah, we figured.

Climate change has rippled through everything, adding volatility to insurance rates. While mollifying the red-polo-and-khaki set is a challenge, it does have its silver linings.

A home built to resist wildfire, hurricanes, and flooding is quite simply, a better-built home. More durable, more valuable, more reassuring. And as a result… more insurable.

The marketplace is filling with products to answer the call, making “insurance-approved” the new gold standard.

Subscribe to the

DRILL DOWN

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.